Number of the Week: $25 billion (explanation below)

Hundreds of thousands of words have been expended this week to explain the GameStop Götterdämerung, too many of them in service of an “investor insurgents vs. incumbents” frame that never felt right (more on this below). But the most striking feature of this tumultuous week was watching one of the world’s most valuable fintech companies attempt suicide. Robinhood for years has sent signals that it misleads its customers, bamboozles unsophisticated investors, and lacks the technological chops needed to maintain the colossus it has created. This week, those longstanding flaws not only roared back, but threatened the firm’s presumed IPO and indeed its very survival.

In a few short years, Robinhood amassed millions of active users, many of whom have used the platform to buy shares in GameStop, AMC and other stocks that have been sold short by hedge funds and other institutional investors. Trading in these “meme stocks” got so furious this week that Robinhood and other brokers shut off access to anyone trying to buy them. This not only infuriated Robinhood’s user base, but also suggested that the company was having trouble meeting its obligations. CNBC’s Andrew Ross Sorkin asked Robinhood CEO Vlad Tenev repeatedly whether his firm was having liquidity problems.

“There was no liquidity problem,” Tenev said. The very next day, Robinhood posted on its blog:

We did this because the required amount we had to deposit with the clearinghouse was so large—with individual volatile securities accounting for hundreds of millions of dollars in deposit requirements—that we had to take steps to limit buying in those volatile securities to ensure we could comfortably meet our requirements.

In other words, Robinhood feared it didn’t have enough money to meet its needs—the very definition of a liquidity problem. The problem was quickly addressed, when Robinhood’s investors agreed to plow a billion additional dollars into the company. (Take a moment to contemplate that—how many companies can raise a billion dollars over the lifetime of the firm, let alone overnight?) But a CEO who can’t tell the truth is a bigger issue than the inability to meet a margin call. And that’s hardly Robinhood’s only problem: the notoriously unstable platform was glitching all week, while customer service was AWOL. But the more severe hurdle for Robinhood is the alienation of all those Red-Bull-and-reddit traders it cut off. Robinhood can probably survive the class-action lawsuit, but the fact that 26,000 users joined the suit in a single day is not a sign of a company with satisfied customers. And the level of scrutiny into Robinhood’s business is only going to ratchet up in coming weeks, as Congress and the Biden Administration try to ride the wave of investor anger.

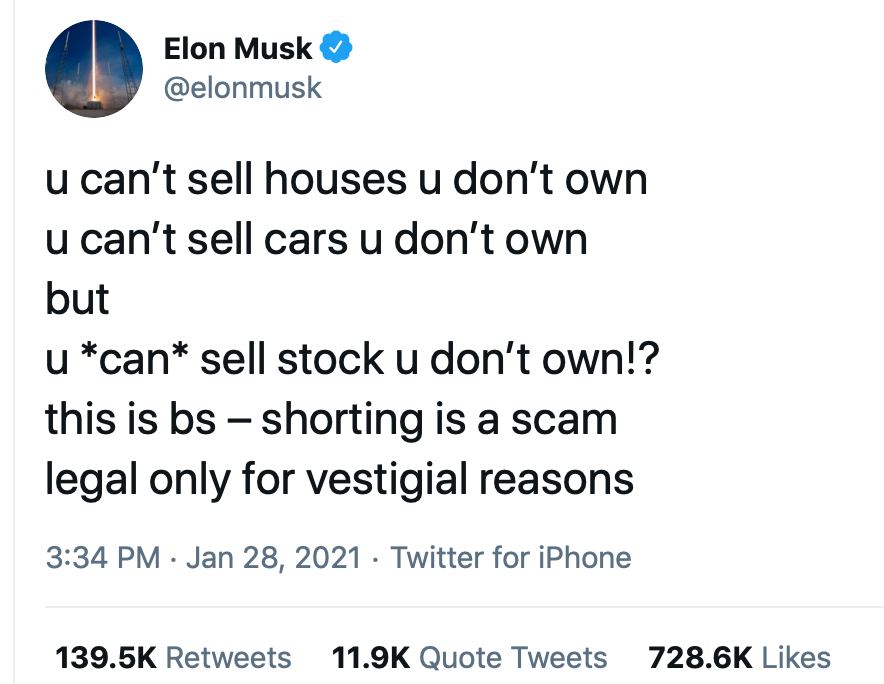

As for regulators, it’s far from clear what positive actions government might take in response to this week’s turmoil, in part because there isn’t a genuine consensus on what the problems are. In the cartoonish populism of the reddit warriors, the problem seems to be the very existence of short-selling, as expressed by Elon Musk’s classic tweet:

Of course, thousands of people every day sell houses they don’t own—it’s called a mortgage—and as Matt Levine points out, Musk became wealthy by selling cars he had yet to build. At any rate, banning short selling altogether seems unlikely to attract Congressional enthusiasm, but it might be possible to cap the percentage of a stock’s outstanding shares that are allowed to be sold short. To Elizabeth Warren, the problem is “a clear distortion in securities markets, with benefits accruing to investors that do not clearly benefit the company's workers, consumers, or the broader economy.” She’s right, but what specifically is supposed to change? Some want to focus on the fact that Robinhood and other brokers cut off buying of GameStop, AMC et al, while others see the semi-coordinated moves to buy GameStop, AMC, et al as the problem. While it’s easy to see how social media could be used to manipulate stock prices, existing securities laws ought to be sufficient to handle that, assuming the government actually wants to enforce those laws and can find clear-cut examples of false statements.

For still others, the problem is the payment for order flow system that Robinhood and other brokerages use to execute trades. As several commentators have noted, Robinhood sells a majority of its trades to Citadel Securities, an arm of one of those evil hedge funds that the rebel traders are purportedly out to destroy. In December, the Securities and Exchange Commission (SEC) fined Robinhood $65 million for making “false and misleading statements” about its use of payment for order flow. It would certainly be possible to ban payment for order flow altogether, and that’s been proposed in the past. That would require a major shift in Robinhood’s business model, and might actually push the retail brokers into trade executions that are even less transparent than today’s system.

Whether effective regulation emerges from this conflagration is hard to predict. But either way, Robinhood seems exposed financially and politically; the company has very little to offer those angry customers that they can’t now get from many competitors. And unlike companies that have been the victim of unfair rumors or aggressive investor tactics, Robinhood’s wounds are entirely self-inflicted.

Governments Hating on Crypto

In all the stock market furor this week, it was easy to miss the remarkable number of officials making sour noises about cryptocurrencies. On January 25, Bank of England governor Andrew Bailey said at an online meeting held by the World Economic Forum that cryptocurrencies are not reliable or stable enough to function as payment. “Have we landed on what I would call the design, governance and arrangements for what I might call a lasting digital currency? No, I don’t think we’re there yet, honestly. I don’t think cryptocurrencies as originally formulated are it,” Bailey said.

But that’s mild in comparison to India, which is preparing to reinstate its ban on private cryptocurrencies, according to a parliamentary bulletin summarizing upcoming legislation. The bill’s ban is part of a plan for an official digital currency to be issued by India’s central bank—but that has to be at least a year away. Crypto bulls will tell you that, on a technological level, enforcement of such a ban is impossible; nonetheless, a ban would likely shut down Indian exchanges like Unocoin. FIN has noted before that government-backed digital currencies create competition for existing cryptocurrencies; increasingly that competition seems to be getting fiercer.

FINvestments

🦈Number of the Week: Brazil’s Nubank raised a $400 million Series G (!) round this week, at an eye-popping valuation of $25 billion. Measured by number of customers and app downloads, Nubank is now the largest digital bank in the world.

🦈You might have had a terrible 2020, but for insurtech it was the best year ever. Last year, $7.1 billion was invested in insurtech companies through 377 deals—a 12% increase in funding and a 20% increase in deals over 2019.

This column originally ran in James Ledbetter's FIN. To subscribe to his weekly newsletter, click here.