A dog is for life, not just for Christmas.

If you are from the United Kingdom, that pithy adage needs no explanation. For everyone else: in 1978, the charity then known as the National Canine Defence League issued a television ad that went viral, in whatever way that happened pre-Internet, and became an international cause. (The Australian singer Sia, for example, riffed on it in her 2017 hit Puppies Are Forever.) The now-iconic campaign was intended to reduce the number of dogs that were bought impulsively in pet shops as holiday gifts, and then returned to overwhelmed charity pounds. But it also suggested a Fezziwig capacity for Brits (and of course others) to splurge during the Christmas season and later regret.

That holiday spendthrift tendency reared its red-inked head this week. The British comparison shopping site Compare The Market released survey data showing that 44 percent of British adults who used Buy Now, Pay Later (BNPL) plans for Christmas shopping now fear that they can’t pay their debts without borrowing more money. The survey coincided with the release of a BNPL report from the Financial Conduct Authority (FCA), and increasing public concern that BNPL can get consumers into trouble; Labour MP Stella Creasy has recently labeled BNPL “a financial scandal waiting to happen,” and called for stricter regulation of the growing sector (more on this below).

BNPL, for those unfamiliar, is essentially an installment plan; instead of paying $150 for a jacket all at once, the customer is given the option of making, say, four payments of $37.50. As long as the money is paid back on time, the service is usually free.

BNPL is one more example of fintech’s “COVID accelerant” documented in the first installment of FIN—indeed, it might be the biggest. “The use of BNPL products nearly quadrupled in 2020 and is now at £2.7 billion (about $3.7 billion), with 5 million people using these products since the beginning of the coronavirus pandemic,” the FCA report said. The entire population of the UK is about 67 million, and presumably children aren’t using BNPL, so we’re talking about a large chunk of the British population. Some UK surveys put the number at 37%, with even higher usage among Generation Z (50%) and millennials (54%). A study found that the average 18-to-24-year-old in the UK owes almost £247 (about $340) to BNPL companies, significantly more than older shoppers. On the whole, these younger consumers tend to have fewer savings than those in Generation X and older, and so their inability to pay Christmas bills could have serious consequences.

Klarna is by far the BNPL market leader in the UK, followed by My Argos Card and Clearpay. On one level, having users fall behind on payments could be helpful to these companies, because they get to tack on fees that rival or even exceed what credit cards charge. But in the long run that could backfire if consumers turn away from BNPL.

Stricter regulation of BNPL seems certain. “Changes are urgently needed: to bring BNPL into regulation to protect consumers; to ensure that there is secure provision of debt advice to help all those who may need it; and to maintain a sustained regulatory response to the pandemic,” said the FCA report.

At least in public, Klarna agrees. In a blog post this week, the company said:

It is essential that regulation is modern, proportionate and fit for purpose, reflecting both the digital nature of transactions and evolving consumer preferences. Given the existing regulation in this area is nearly fifty years old, a comprehensive update to this entire framework reflecting consumers’ changing needs is in our view the right thing to do….

We would like to see robust regulation for the buy now pay later sector that:

Guarantees transparency for consumers to ensure they fully understand what interest, late fees and / or payment schedules they are committing to (though Klarna charges no interest or fees on our most popular products).

Ensures all providers perform strict eligibility checks, and have access to accurate information on consumers’ use of these products, so the services are only offered to consumers who can pay.

Gives consumers the same purchase protection regardless of the type of product they’ve used, whether this relates to the quality of the product and right to return, or to the help available for unexpected financial hardship.

Enables consumers to take complaints to the Financial Ombudsman Service or similar service regardless of whether a product charges interest or not.

Might the same pattern be occurring in the US? BNPL usage is proportionally smaller in America, but the heavy participation of millennials and Gen Z is similar. On Monday, Credit Karma released a survey showing that a little more than 40% of American adults have used a BNPL service; of those, 38% have been late on a payment at least once, usually causing their credit scores to drop. And consider this: shares in Affirm—the biggest US public BNPL company, if you don’t count PayPal—began tumbling on Tuesday (the day that report and survey were released) and by Friday’s close of trade were down $10 a share, during a time when the Nasdaq as a whole was rising.

(Canine hat tip to Ben Schott.)

Fintech Fails the PPP Test

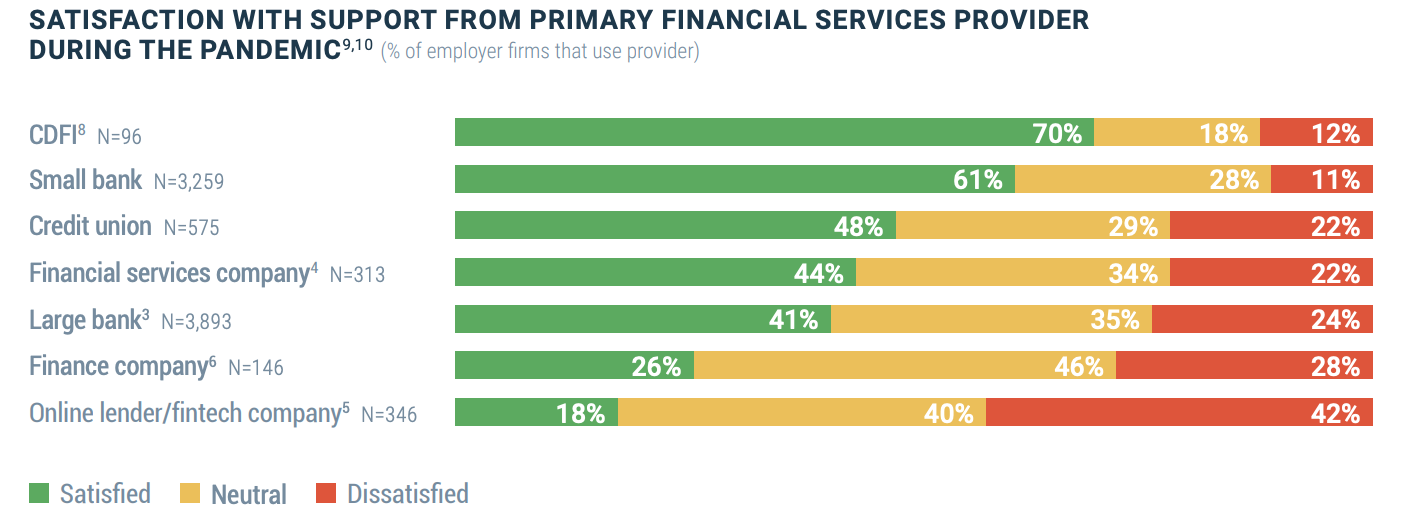

One of the fundamental premises of fintech is that it provides customers with faster, more convenient access to money than traditional financial institutions usually can. And with a situation like the Payroll Protection Program (PPP), delivering money quickly and reliably makes a big difference. According to a Federal Reserve survey issued this week, PPP borrowers in 2020 were none too impressed:

That’s a big discrepancy, and doesn’t make fintech companies look great. One reason that small businesses grade fintech companies so poorly may be that many don’t have their records sufficiently digitized to feed easily into fintech apps. Even so, small businesses represent a vital market for fintech, and alienating them at a time of urgent need is a big mistake. Looking beyond PPP to lending in general, the Fed survey found that small business satisfaction with online banks/fintech has fallen from a peak of 39% in 2017 to 25% in 2020. Fintech has got to fix this customer problem if it expects to continue to expand.

FINvestments

🦈Number of the Week: The implied value of SoFi right now is about $20 billion. That is, when it was announced in January that the fintech lender would go public via a SPAC created by Chamath Palihapitiya, the value of the deal was put at $8.65 billion. The deal has yet to close, but shares of the SPAC have recently traded at 2.3 times their initial price, which comes out to about $20 billion. It’s possible, of course, that once the deal is final, the shares will go down—except, in this market, does anything go down for long?

🦈This week the fintech mortgage servicer Valon announced a $50 million Series A round led by Andreessen Horowitz. A couple of interesting things stand out about this company: 1) We are likely to witness a lot of churn in the mortgage market this year; and 2) Valon is taking on a true industry colossus; Black Knight’s technology currently controls about half the market. There is a real opportunity here for Valon to grow quickly and give consumers more competition.

This column originally ran in James Ledbetter's FIN. To subscribe to his weekly newsletter, click here.